1) A Review by Seix Investment Advisors LLC�

FIRST QUARTER 2016

RIDGEWORTH INSIGHTS:

INVESTMENT GRADE FIXED INCOME

EXECUTIVE SUMMARY

•

Central bank actions calmed investors’ fears, leading to a

rebound in riskier bonds.

We think deflationary forces in the global economy will

keep interest rates low for the foreseeable future.

Perry Troisi

Chief Investment Officer

and Chairman,

Seix Investment Advisors

•

•

James F. Keegan

Investors were concerned about global growth and

fled risk assets during the first six weeks of the quarter,

causing Treasuries to rally.

Managing Director,

Seix Investment Advisors

Senior Portfolio Manager,

RidgeWorth Investments

Senior Portfolio Manager,

RidgeWorth Investments

Michael Rieger

Seth Antiles, PhD

Managing Director,

Seix Investment Advisors

Managing Director,

Seix Investment Advisors

Carlos Catoya

Jon Yozzo

Head of Investment Grade

Credit Research,

Seix Investment Advisors

Head of Investment Grade

Corporate Bond Trading,

Seix Investment Advisors

Senior Portfolio Manager,

RidgeWorth Investments

Portfolio Manager,

RidgeWorth Investments

Senior Portfolio Manager,

RidgeWorth Investments

Portfolio Manager,

RidgeWorth Investments

RIDGEWORTH FUNDS

RidgeWorth Seix Core Bond

RidgeWorth Seix Corporate Bond

RidgeWorth Seix Limited Duration

RidgeWorth Seix Short-Term Bond

RidgeWorth Seix Total Return Bond

RidgeWorth Seix U.S. Government Securities

Ultra-Short Bond

RidgeWorth Seix U.S. Mortgage

RidgeWorth Seix Ultra-Short Bond

The first quarter was a tale of two markets. Investors fled

risk during the first six weeks of the year, causing Treasury

securities to rally and credit to underperform. The situation

partially reversed itself midway through the first quarter:

Investors became more comfortable with risk, helping credit

sectors recover while Treasury yields remained near the lows

in terms of yields.

�

2) �

FIRST QUARTER 2016 | PAGE 2

RIDGEWORTH INSIGHTS: INVESTMENT GRADE FIXED INCOME

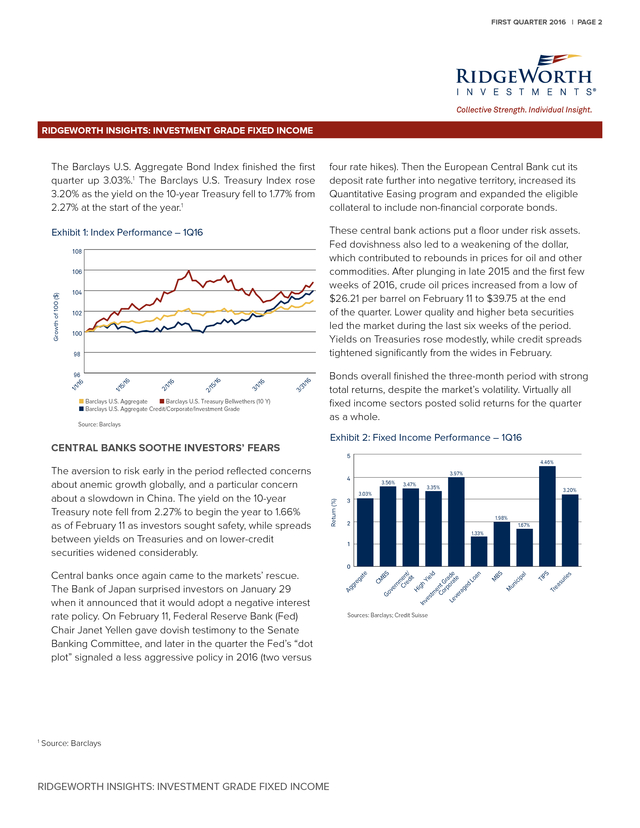

The Barclays U.S. Aggregate Bond Index finished the first

quarter up 3.03%.1 The Barclays U.S. Treasury Index rose

3.20% as the yield on the 10-year Treasury fell to 1.77% from

2.27% at the start of the year.1

four rate hikes). Then the European Central Bank cut its

deposit rate further into negative territory, increased its

Quantitative Easing program and expanded the eligible

collateral to include non-financial corporate bonds.

Exhibit 1: Index Performance – 1Q16

These central bank actions put a floor under risk assets.

Fed dovishness also led to a weakening of the dollar,

which contributed to rebounds in prices for oil and other

commodities. After plunging in late 2015 and the first few

weeks of 2016, crude oil prices increased from a low of

$26.21 per barrel on February 11 to $39.75 at the end

of the quarter. Lower quality and higher beta securities

led the market during the last six weeks of the period.

Yields on Treasuries rose modestly, while credit spreads

tightened significantly from the wides in February.

108

Growth of 100 ($)

106

104

102

100

98

/16

31

3/

6

1/1

3/

/16

15

2/

6

1/1

2/

16

5/

1/1

1/1

/16

96

I Barclays U.S. Aggregate

I Barclays U.S. Treasury Bellwethers (10 Y)

I Barclays U.S. Aggregate Credit/Corporate/Investment Grade

Source: Barclays

Bonds overall finished the three-month period with strong

total returns, despite the market’s volatility. Virtually all

fixed income sectors posted solid returns for the quarter

as a whole.

Exhibit 2: Fixed Income Performance – 1Q16

CENTRAL BANKS SOOTHE INVESTORS’ FEARS

4.46%

3.97%

4

3.56%

3.47%

3.35%

3.20%

3.03%

Return (%)

The aversion to risk early in the period reflected concerns

about anemic growth globally, and a particular concern

about a slowdown in China. The yield on the 10-year

Treasury note fell from 2.27% to begin the year to 1.66%

as of February 11 as investors sought safety, while spreads

between yields on Treasuries and on lower-credit

securities widened considerably.

5

3

1.98%

2

1.67%

1.33%

1

1

Source: Barclays

RIDGEWORTH INSIGHTS: INVESTMENT GRADE FIXED INCOME

Sources: Barclays; Credit Suisse

TI

PS

Tr

ea

su

rie

s

un

ici

pa

l

M

BS

M

BS

er

nm

Cr en

ed t/

it

Hi

gh

In

ve

Yi

el

stm

d

e

Co nt G

rp ra

or de

Le

at

ve

e

ra

ge

d

Lo

an

CM

Go

v

Ag

gr

eg

at

e

0

Central banks once again came to the markets’ rescue.

The Bank of Japan surprised investors on January 29

when it announced that it would adopt a negative interest

rate policy. On February 11, Federal Reserve Bank (Fed)

Chair Janet Yellen gave dovish testimony to the Senate

Banking Committee, and later in the quarter the Fed’s “dot

plot” signaled a less aggressive policy in 2016 (two versus

�

3) �

FIRST QUARTER 2016 | PAGE 3

Please contact 866.595.2470 or visit www.ridgeworth.com for more information.

OUTLOOK: STILL LOWER FOR LONGER

We expect deflationary pressures—including excessive

debt, excess global capacity, slowing productivity, aging

demographics, tepid potential U.S. growth and China’s

transition from an industrial to a consumer economy—to

continue to exceed inflationary pressures. The threat of

deflation or disinflation is likely to cause central banks to

remain highly accommodative for the foreseeable future,

and to keep long-term interest rates low for an extended

period of time.

The U.S. and global economies remain weak. We see a

one-in-two likelihood of a global recession—defined as

global growth below 3%—in the next 12 months, and a

one-in-three chance of recession for the U.S. economy.

Given that economic backdrop and global deflationary

pressures, we expect no more than one interest rate hike

in the United States this year, and in fact, we think the

Barclays Govt/Credit Bond Index is an unmanaged Index that tracks the performance

of US Government and corporate bonds rated investment grade or better, with

maturities of at least one year.

Barclays Municipal Bond Index is an unmanaged index that is considered

representative of the broad market for investment grade, tax-exempt bonds with a

maturity of at least one year.

Barclays U.S. Aggregate Bond Index is an unmanaged index of U.S. bonds, which

includes reinvestment of any earnings and is widely used to measure the overall

performance of the U.S. bond market.

Barclays U.S. Mortgage Backed Securities Index is an unmanaged index that

measures the performance of investment grade fixed-rate mortgage-backed

passthrough securities of GNMA, FNMA, and FHLMC.

Barclays U.S. Corporate High Yield Bond Index is an unmanaged market valueweighted index that covers the universe of fixed rate, non-investment grade debt.

Barclays U.S. Corporate Investment Grade Index is a widely recognized index that

tracks the performance of investment grade bonds.

Barclays U.S. CMBS Investment Grade Index measures the market of conduit and

fusion CMBS deals with a minimum current deal size of $300mn. The index is

divided into two subcomponents: the U.S. Aggregate-eligible component, which

contains bonds that are ERISA eligible under the underwriter’s exemption, and the

non-U.S. Aggregate-eligible component, which consists of bonds that are not ERISA

eligible. The U.S. CMBS Investment Grade Index was launched on January 1, 1997.

Barclays US Treasury Inflation-Protection Securities (TIPS) Index consists of inflationprotection securities issued by the US Treasury. They must have at least one year

until final maturity and at least $250 million par amount outstanding. They are rated

investment grade by at least two of the following ratings agencies: Moody’s, S&P,

Fitch. They must be fixed rate, dollar denominated and non-convertible.

Barclays U.S. Treasury Index includes public obligations of the U.S. Treasury with a

remaining maturity of one year or more.

Credit Suisse Leveraged Loan Index is a market-weighted index that tracks the

performance of institutional leveraged loans.

Trade-Weighted U.S. Dollar Index is a measure of the value of the United States

dollar relative to other world currencies.

Investors cannot invest directly in an index.

federal funds rate is more likely to fall back to 0% than to

rise to 1%. We expect the 10-year Treasury note to yield

between 1.5% to 2.0% during the next 12 months, but we

would not be surprised if the yield falls closer to 1%.

China and Europe present major risks. We think China will

have to weaken its currency, which could destabilize the

markets. We believe Europe is stagnating economically,

which could polarize politics and threaten social stability, a

situation worsened by the refugee crisis.

We expect oil production to decrease in the coming

months, bringing inventories closer to the five-year

average by year-end and supporting higher prices. As a

result, we see value in bonds issued by well-run energy

companies with the financial strength to weather market

distress.

Beta is a measure of the volatility of a security or a portfolio in comparison to its

benchmark.

Credit Spreads are the difference between the yields of sector types and/or

maturity ranges.

Investment Risks:

Bonds offer a relatively stable level of income, although bond prices will fluctuate

providing the potential for principal gain or loss. Intermediate-term, higher-quality

bonds generally offer less risk than longer-term bonds and a lower rate of return.

Generally, a fund’s fixed income securities will decrease in value if interest rates rise

and vice versa. Mortgage-backed investments involve risk of loss due to prepayments

and, like any bond, due to default. Because of the sensitivity of mortgage-related

securities to changes in interest rates, a fund’s performance may be more volatile

than if it did not hold these securities. U.S. Government guarantees apply only to the

underlying securities of a fund’s portfolio and not a fund’s shares.

The views expressed herein are as of the quarter-end specified. This information is

general in nature, provided as general guidance on the subject covered, and is not

intended to be authoritative. It is subject to change without notice as market conditions

change, and is not intended to predict the performance of any individual security,

market sector, or RidgeWorth Fund. All information contained herein is believed to

be correct, but accuracy cannot be guaranteed. Investors are advised to consult with

their investment professional about their specific financial needs and goals before

making any investment decision.

Before investing, investors should carefully read the

prospectus or summary prospectus and consider the fund’s

investment objectives, risks, charges and expenses. Please

call 888.784.3863 or visit ridgeworth.com to obtain a

prospectus or summary prospectus, which contains this and

other information about the funds.

©2016 RidgeWorth Investments. All rights reserved. RidgeWorth Investments is

the trade name for RidgeWorth Capital Management LLC, an investment adviser

registered with the SEC and the adviser to the RidgeWorth Funds. RidgeWorth

Funds are distributed by RidgeWorth Distributors LLC, which is not affiliated with

the adviser. Seix Investment Advisors LLC is a registered investment adviser with

the SEC and a member of the RidgeWorth Capital Management LLC network of

investment firms. All third party marks are the property of their respective owners.

�

4) �

FIRST QUARTER 2016 | PAGE 4

ridgeworth.com | 866.595.2470

3333 Piedmont Road, NE

�Suite 1500

A

� tlanta, GA 30305

ABOUT RIDGEWORTH INVESTMENTS

RidgeWorth Investments—a global investment management firm headquartered in Atlanta, Georgia with approximately $37.9 billion

in assets under management as of March 31, 2016—offers investors access to a select group of boutique investment managers and

subadvisers. RidgeWorth wholly owns three boutiques: Ceredex Value Advisors LLC, Seix Investment Advisors LLC and Silvant Capital

Management LLC, and holds a minority ownership in Zevenbergen Capital Investments LLC. WCM Investment Management and Capital

Innovations, LLC serve as subadvisers to the RidgeWorth Funds. Through these six investment managers, RidgeWorth offers a wide variety

of fixed income and equity disciplines, providing investment management services to a growing client base that includes institutional,

individual and high net worth investors.

For more information about RidgeWorth, its boutiques and its subadvisers, visit ridgeworth.com.

ABOUT SEIX INVESTMENT ADVISORS LLC

Seix Investment Advisors, one of RidgeWorth’s investment management boutiques, has exclusively focused on managing fixed income

assets since 1992. Seix seeks to generate competitive absolute and relative risk-adjusted returns over the full market cycle through

a bottom-up focused, top-down aware process. Seix employs multi-dimensional approaches based on strict portfolio construction

methodology, sell disciplines and trading strategies with prudent risk management as a cornerstone.

For more information about Seix, visit seixadvisors.com.

RFRI-INVG-0316

�