1) Tax Planning Guide 2015 Year-End

2) Contents MOSS ADAMS 2015 Year-End Tax Planning Guide | Introduction 4 How to Use This Guide 5 Tax Planning for Individuals 6 8 Personal Income Tax Stock Option Planning Capital Gains Alternative Minimum Tax Qualified Small Business Stock 7 9 10 11 College Education Planning 12 Real Estate Holdings 14 Net Investment Income Tax and Additional Medicare Tax 12 Tax Issues for Same-Sex Couples 15 Retirement Planning 22 Health Care Reform 25 Estate and Gift Planning Charitable Giving Wealth Management International Considerations 16 19 23 24 Tax Planning for Business Owners and Businesses 27 Highlight: Self-Rental Planning 28 Depreciable Real Estate 29 and Pitfalls Highlight: The Highway Act and Business Equipment Business Credits Tangible Property Regulations Employee Benefits Health Care Reform 28 30 31 32 International Tax 33 Ownership Transition 35 Entity Structure Exit Planning Sales and Acquisitions 34 34 36 37 2

3) MOSS ADAMS 2015 Year-End Tax Planning Guide | Looking Forward: Potential Tax Proposals 39 Permanent, Higher Section 179 39 State Versus Sales Tax Deductions 39 Expensing Permanent Research Tax Credit Maximum Tax Benefit for Retirement Savings Contributions Backdoor Roth IRA Conversions Stretch IRAs Estate Tax Other Proposed Changes 39 39 39 40 40 40 Contributors 41 Contact Us 44 About Moss Adams 44 3

4) Introduction “Someone’s sitting in the shade today because someone planted a tree a long time ago.” Long before Warren Buffett made this statement 25 years ago, the same three keys to financial success were already well established: a goal, a plan to achieve that goal, and timing. Just by glancing at this year-end guide, you’ve taken the first step toward your goals, and the timing couldn’t be better for reevaluating your plan. The last few months of the year are ideal for discussing with your advisor whether you, your family, and your business are on track to achieving your objectives. Starting with tax issues is natural when you meet with your advisor, but also take time for a holistic discussion. How will the past year’s life events influence your income taxes? Buying a new home, contributing to your company’s 401(k), leaving your job to start a new business—these all have an impact on not only your income taxes but also your overall plan. How will buying a home affect your living trust and overall estate plan? If your company offers a Roth 401(k), will it allow you to meet your retirement planning needs more effectively than a traditional 401(k)? If you leave your employer, will you receive a severance package or have to decide on stock option exercises? How will starting a new business impact your cash flow and financial plan? A plethora of legislative and economic issues hover over the financial landscape. The provisions of the Affordable Care Act will affect both your family life and your business, taking the form of penalties for noncompliance and new reporting methods. New foreign tax issues highlight how living and working in a global economy requires a very detailed MOSS ADAMS 2015 Year-End Tax Planning Guide | 4 international road map. The tangible property regulations have significant impacts on business owners and their asset capitalization policies, and these same rules may apply in your personal life as well. Throughout this planning guide, we’ll help bring clarity to these and other important issues. Also essential is generational planning, including the transfer of assets, your estate and gift plan, any charitable contributions, and business succession. Discuss with your advisor the transfer of your assets to the next generation, and review your estate and gift plans to address any changes in tax laws so that your wishes are accurately documented and can be executed successfully. Work with your advisor to cultivate a charitable giving strategy that’s tailored to your family’s needs, is rewarding to you, and benefits society in a way you value. And finally, approach business succession strategies with an open mind so that family and other central stakeholders can maintain and grow the commercial value you’ve developed. As advisors, we think of ourselves as being a bit like doctors: we’re here to help you make informed decisions about the health of your finances and future estate, but we can only do so when we know what’s happening within your life, your family, and your business. Use this guide as a starting point for discussions and planning when you meet your advisor. By working together, we can help you plan so you’ll be sitting in the shade of your tree for many years to come.   TABLE OF CONTENTS >

5) How to Use This Guide MOSS ADAMS 2015 Year-End Tax Planning Guide | 5 This guide contains two sections that discuss key tax planning opportunities for the 2015 tax year. The first covers topics relevant for individuals, and the second covers topics for businesses and their owners. As you read through this guide, take note of opportunities that may be relevant to you, your business, and your family. Your Moss Adams advisor will be able to discuss those opportunities with you in greater detail, helping you decide which to pursue and how so that you can hold on to more of what you’ve earned and maintain a foundation for your long-term financial health. Like a tree, some of the tactics discussed here take time to produce shade. Your window of opportunity grows only smaller as the tax year-end approaches, so the sooner you and your advisor meet and implement a strategy, the greater the likelihood you’ll be able to reap the benefit. Remember that the strategies discussed in this guide are based on current federal tax law, which is subject to change in light of our ever-evolving tax code. To stay up to date on key topics, visit www.mossadams.com/insights and subscribe to our e-mail alerts and articles, which will keep you in the loop on key developments and opportunities. And finally, keep state tax laws in mind as well, since these too may impact your tax and financial planning.  TABLE OF CONTENTS >

6) Tax Planning for Individuals MOSS ADAMS 2015 Year-End Tax Planning Guide | 6 This section covers tax planning items relevant to individual taxpayers, but those who are business owners should also review the contents of the second section, Tax Planning for Business Owners and Businesses (see page 27), since certain business-related tax issues can impact your personal income tax planning. Tax Planning for Individuals Personal Income Tax Stock Option Planning Capital Gains Alternative Minimum Tax Qualified Small Business Stock What Qualifies as QSBS? 7 8 9 10 11 11 College Education Planning 12 Real Estate Holdings 14 Net Investment Income Tax and Additional Medicare Tax Tax Issues for Same-Sex Couples Estate and Gift Planning The Highway Act and Valuation Opportunities Lifetime Gifts Low Interest Rate Gifting and Trust Entity Structures Developing or Updating Your Estate Plan 12 15 16 16 17 17 Charitable Giving Charitable Giving as Part of Your Overall Estate Plan Document Your Charitable Contributions Retirement Planning Wealth Management Investment Management and Strategy Personal Financial Planning Insurance International Considerations Health Care Reform 19 20 21 22 23 23 24 24 24 25 17 19 TABLE OF CONTENTS >

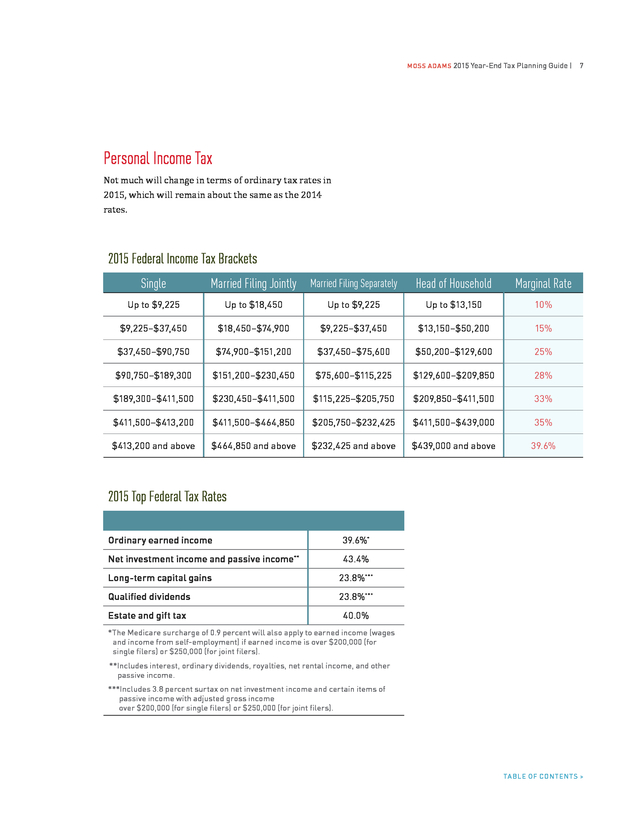

7) MOSS ADAMS 2015 Year-End Tax Planning Guide | 7 Personal Income Tax Not much will change in terms of ordinary tax rates in 2015, which will remain about the same as the 2014 rates. 2015 Federal Income Tax Brackets Single Married Filing Jointly Married Filing Separately Head of Household Marginal Rate Up to $9,225 Up to $18,450 Up to $9,225 Up to $13,150 10% $9,225–$37,450 $18,450–$74,900 $9,225–$37,450 $13,150–$50,200 15% $37,450–$90,750 $74,900–$151,200 $37,450–$75,600 $50,200–$129,600 25% $90,750–$189,300 $151,200–$230,450 $75,600–$115,225 $129,600–$209,850 28% $189,300–$411,500 $230,450–$411,500 $115,225–$205,750 $209,850–$411,500 33% $411,500–$413,200 $411,500–$464,850 $205,750–$232,425 $411,500–$439,000 35% $413,200 and above $464,850 and above $232,425 and above $439,000 and above 39.6% 2015 Top Federal Tax Rates Ordinary earned income 39.6%* Net investment income and passive income** 43.4% Long-term capital gains 23.8%*** Qualified dividends 23.8%*** Estate and gift tax 40.0% *The Medicare surcharge of 0.9 percent will also apply to earned income (wages and income from self-employment) if earned income is over $200,000 (for single filers) or $250,000 (for joint filers). **Includes interest, ordinary dividends, royalties, net rental income, and other passive income. ***Includes 3.8 percent surtax on net investment income and certain items of passive income with adjusted gross income over $200,000 (for single filers) or $250,000 (for joint filers). TABLE OF CONTENTS >

8) MOSS ADAMS 2015 Year-End Tax Planning Guide | IS YOUR SIDE BUSINESS A HOBBY? Taxpayers and the IRS don’t always see eye to eye when determining whether a side business is a considered a hobby or a trade or business. The tax ramifications of being labeled as a hobby can be quite substantial: As a general rule, a trade or business can deduct all directly related business expenses. A taxpayer engaged in a hobby, on the other hand, can deduct expenses only to the extent of income. Furthermore, these expenses are reported as miscellaneous itemized deductions, which are subject to further limitations on your Schedule A and nondeductible for AMT purposes. Your specific facts and circumstances will determine whether you’re operating a trade or business as opposed to a hobby. The IRS regulations give nine factors to help determine how to classify your side business, and they also provide a safe harbor in which any activity that has had a profit for three of the last five will be treated as trade or business, not a hobby. The safe harbor’s downside is that it doesn’t apply until you’ve had three profitable years. These rules are complex and should be analyzed with the help of your advisor. If you haven’t yet considered how to classify your side business, sit down with your advisor to help make and document your determination. 8 Capital Gains The maximum 2015 rates for capital gains and qualified dividends remain at 20 percent. If your taxable income falls below the following thresholds, then your maximum capital gains rate will instead be 15 percent: • For married couples filing jointly, $464,850 • For married couples filing separately, $232,425 • For heads of household, $439,000 • For single filers, $413,200 Whether you pay the 15 or 20 percent rate, that amount could potentially rise an extra 3.8 percent if your situation also qualifies for the net investment income tax (NIIT). (For more on the NIIT, see page 12). With that in mind, here are some planning actions you may want to take: • Make use of unrealized portfolio losses. Review your investment accounts for unrealized loss positions; now may be a good time to use them to your advantage. Work with your investment advisor to implement these tax-loss harvesting strategies and rebalance your investment portfolio with a priority on tax-efficient investments. • Donate securities with appreciated capital gains. If you plan to make charitable donations, consider giving appreciated capital gain assets you’ve held for more than a year instead of cash. In doing so, you reduce the amount of your income that would be subject to capital gains tax and the 3.8 percent NIIT, earning a charitable deduction for the full fair-market value of the assets along the way. • Time expenditures to shift deductions. By making expenditures sooner or later than you otherwise planned, you may be able to shift the TABLE OF CONTENTS >

9) MOSS ADAMS 2015 Year-End Tax Planning Guide | corresponding deduction from a year when you can’t use them into a year when you can. Note that your deduction will be reduced or lost if your adjusted gross income (AGI) exceeds a certain threshold. • Bunch your medical expenses together. To the extent you can control the timing of your medical expenses, group them into the same tax year so they’ll exceed the yearly threshold to deduct them. For taxpayers age 65 and under, the threshold is 10 percent of your AGI; for taxpayers above age 65, the threshold is 7.5 percent. Note that medical expenses aren’t reduced by the itemized deduction phaseout. • Time year-end property and state income tax payments. If you pay your fourth-quarter estimated state income tax and your real estate property tax in December 2015, you’ll be able to deduct them against your 2015 taxes. If instead you pay them in January 2016, then you would claim the deduction on your 2016 return. Some states do penalize taxpayers for deferring these taxes to the following year, but often the value of the deduction more than offsets the penalty. Be sure to discuss the timing of these payments with your Moss Adams advisor because of their interplay with both the alternative minimum tax (AMT) and NIIT. Alternative Minimum Tax The AMT applies to taxpayers who might otherwise pay little or no regular tax because they’re using certain deductions. Essentially, you’ll pay whichever is higher: regular tax or AMT. When it comes to calculating AMT, many items you’re used to deducting aren’t deductible; in fact, they only increase your risk of paying AMT instead of regular income tax. 9 A combination of the following factors—the effects of which will vary depending on your individual tax situation—could trigger an AMT liability: • Large deductions for state and local income or sales tax (particularly in high-tax states, such as California and Oregon) • A large portion of total income from long-term capital gains • The exercise of incentive stock options (ISOs) • Personal property or real estate taxes • Investment advisory fees • Accelerated depreciation adjustments and related gain or loss differences • Employee business expenses • Tax-exempt interest on certain private activity bonds • Interest on home equity loans that aren’t being used to acquire or improve your residence To reduce your AMT exposure: • Defer tax payments. If you’re perpetually subject to AMT, carefully consider deferring your payments to the period that provides the greatest tax benefit. Common examples include the timing of property tax payments or fourth-quarter state income taxes. Check with your advisor before implementing this strategy to understand how it will impact your tax liability under the NIIT. • Plan before exercising ISOs. Consult your Moss Adams advisor before you exercise ISOs to avoid unexpected tax consequences, since doing so might trigger an AMT liability and increase your overall tax liability (see page 10). • Accelerate income. You can potentially mitigate the impact of the AMT by accelerating income into a year when your regular tax and AMT would be TABLE OF CONTENTS >

10) MOSS ADAMS 2015 Year-End Tax Planning Guide | 10 the same. You’ll pay tax sooner, but your effective tax rate will be only 26 or 28 percent on the accelerated income compared to 39.6 percent when you’re not subject to AMT. • Maximize mortgage deductions. The maximum mortgage principal amounts are $1 million for original acquisition debt and $100,000 for home equity debt. If you anticipate paying AMT and plan to either purchase a new residence or make improvements to your current residence, consider obtaining the maximum mortgage available if you might otherwise need to borrow the funds later on. Under AMT rules, interest expenses are deductible only on the debts you incur to acquire, construct, or rehabilitate a residence. Additionally, interest expenses on second mortgages are deductible only if they’re used for substantial improvements to an existing residence. Stock Option Planning If your compensation package includes stock options, paying close attention to how and when you exercise your options and sell your stock can have a substantial impact on your personal tax liability. Here are a few ways you can control the tax impact: • Exercise ISOs up to AMT crossover. Assuming you’re not already in AMT (see page 9), consider exercising any incentive stock options up to the AMT crossover point—the point at which you’ll begin to pay AMT on any additional ISO exercises. By purchasing stock only up to the crossover point, you’re essentially exercising those shares tax-free. Exercise any more, and you’ll end up paying AMT. • Sell publicly traded shares at a loss. If your ISO is for a publicly traded stock, the stock price has gone down, you’ve held it for less than a year, and it doesn’t look like it will recover soon, then consider selling the stock. This will trigger a disqualifying disposition that makes your gains taxable as ordinary income, freeing you from paying AMT on the spread when you exercised. This works best when done within the same tax year (that is, when you exercise early in the year and disqualify by year-end if the stock goes down). • Exercise nonqualified stock options. If you expect to be subject to AMT for 2015 and don’t expect any AMT credit carryforward, consider exercising nonqualified stock options. In doing so, the accelerated ordinary income may be taxed at 28 percent (the AMT marginal rate) compared to 39.6 percent for taxpayers in the highest marginal federal tax bracket. Plus, all future appreciation will be considered a capital gain. Be sure to weigh your potential tax savings against the opportunity cost of accelerating the income, taking into account the time value of money. • File an 83(b) election and exercise early. If you’ve received an option grant subject to vesting restrictions and the value of the shares is still equal to the grant price (or strike price), consider exercising your options early, assuming early exercise is available. This will start the capital gains holding clock, getting you to the preferential tax rate on long-term gains sooner. If you do choose early exercise, don’t forget to file an 83(b) election form with the IRS, because there’s a time limit for doing so. Ask your advisor if you have any questions about this. TABLE OF CONTENTS >

11) MOSS ADAMS 2015 Year-End Tax Planning Guide | 11 STOCK OPTION? OR RIGHT TO FUTURE PAYMENT? In light of the Tax Court case David S. Stout and Crystal A. Stout v. Commissioner of Internal Revenue, it’s important to review the compensation document you received from your employer regarding your stock options. In the Stout case, a software engineer’s employer authorized and instituted a stock equivalent plan, pursuant to which it issued stock incentive units (SIUs) to full-time salaried employees who met certain criteria. The software engineer thought the SIUs he received were ISOs; however, the plan document clearly stated that the SIUs represented only an unsecured promise to pay and that plan participants couldn’t acquire any right, title, or interest in any assets of the company. Therefore, under the court’s opinion, the software engineer received only a right to a future payment. As a result, the engineer was required to report these payments as ordinary income when received. Review any documents you received from your company carefully to avoid a misconception like this one from happening. Qualified Small Business Stock Congress has provided a variety of incentives to encourage taxpayers to invest in small businesses. In the past several years, these incentives have become more generous—to the point where it’s possible to get a complete exemption from federal income tax on gains from the sale of certain qualified small business stock (QSBS). The IRS’s rules surrounding QSBS are strict. In order WHAT QUALIFIES AS QSBS? for an investment to qualify for QSBS tax treatment, each of the following must apply: • It’s stock in a C corporation and was originally issued after August 10, 1993. • The corporation was a domestic C corporation with total gross assets of $50 million or less as of the date the stock was issued. • The taxpayer acquired the stock at its original issue (either directly or through an underwriter) either in exchange for money or other property or as pay for services (other than as an underwriter) to the corporation. • It was issued by a corporation that uses at least 80 percent of its assets (by value) in an active trade or business. • It was held for more than five years. Here’s how to handle your QSBS from a tax perspective: • Exclude a percentage of QSBS gains. Under Section 1202, noncorporate taxpayers can exclude at least 50 percent of the gain recognized on the sale or exchange of QSBS they’ve held for more than five years. For qualifying stock acquired after February 17, 2009, and on or before September 27, 2010, the exclusion percentage is 75 percent. Qualifying stock acquired after September 27, 2010, and before January 1, 2015, can be excluded at 100 percent. Note that for purposes of the AMT calculation, you’ll need to add back 7 percent of the excluded gain unless the stock qualifies for the 100 percent exclusion, in which case there’s no AMT add-back. • Roll over your QSBS gains. You also have the option to roll over the gain from one QSBS to another. A gain on the sale of QSBS that’s been held for more than six months isn’t currently taxed if the proceeds are invested in another QSBS within 60 days of the sale. The rules on this particular provision are complex, so consult your tax advisor. This is a high-level overview, so if you’re purchasing or selling QSBS, again, consult with your tax advisor TABLE OF CONTENTS >

12) MOSS ADAMS 2015 Year-End Tax Planning Guide | 12 on the specifics. Note as well that California taxpayers will have to report 100 percent of the gain on their state returns because California no longer allows an exclusion for QSBS. College Education Planning Higher education is a significant expense for many families, so taking time to consider how you can use related expenses to a tax advantage is well worth the effort. • Claim the American Opportunity Tax Credit. This credit is available for the first four years of qualified expenses paid for undergraduate education. For tax year 2015, you may be able to claim up to $2,500 per student. Of the credit amount you receive, 40 percent is refundable. • Explore other credits and deductions. If you’re paying for postsecondary education and aren’t eligible for the American Opportunity Tax Credit, you may be still eligible for the lifetime learning credit or the tuition and fees deduction. Consult your Moss Adams advisor to determine your eligibility. • Create a Section 529 account. These investment accounts can be used to accumulate funds for college-related expenses. The appreciation on the investments within the account is tax-free for qualified distributions. Under certain elections, taxpayers may contribute up to $70,000 (for single filers) or $140,000 (for married couples) to a Section 529 account over a period of five years without reducing their lifetime gift and estate tax exemption, although you should contact your tax advisor regarding gift tax filing requirements. If you currently maintain college funds in taxable accounts, it may make sense to shift these funds to a Section 529 account, where they won’t generate future taxable income. Net Investment Income Tax and Additional Medicare Tax Now in their third year, the 3.8 percent NIIT and additional 0.9 percent Medicare surtax apply to taxpayers with income above certain thresholds (see table on the following page). The thresholds for the two taxes are nearly the same, but they apply to different types of income. The 0.9 percent additional Medicare tax applies to Federal Insurance Contributions Act wages and selfemployment income. The NIIT equals 3.8 percent of the lesser of the taxpayer’s net investment income or the amount by which the taxpayer’s MAGI exceeds the thresholds. Net investment income includes interest, dividends, capital gains, rents and royalty income, income that isn’t from a trade or business, and any other passive income (meaning the taxpayer doesn’t materially participate in the business). Certain types of income are excluded from net investment income, including wages, self-employment income, active trade or business income, retirement plan distributions, unemployment compensation, Social Security benefits, alimony, interest from tax-free bonds (such as municipal bonds), and Alaska Permanent Fund Dividends. Note that the thresholds aren’t indexed for inflation, which means they haven’t changed from last year or the year before. It also means that inflation alone will cause these taxes to reach increasing numbers of taxpayers over time. TABLE OF CONTENTS >

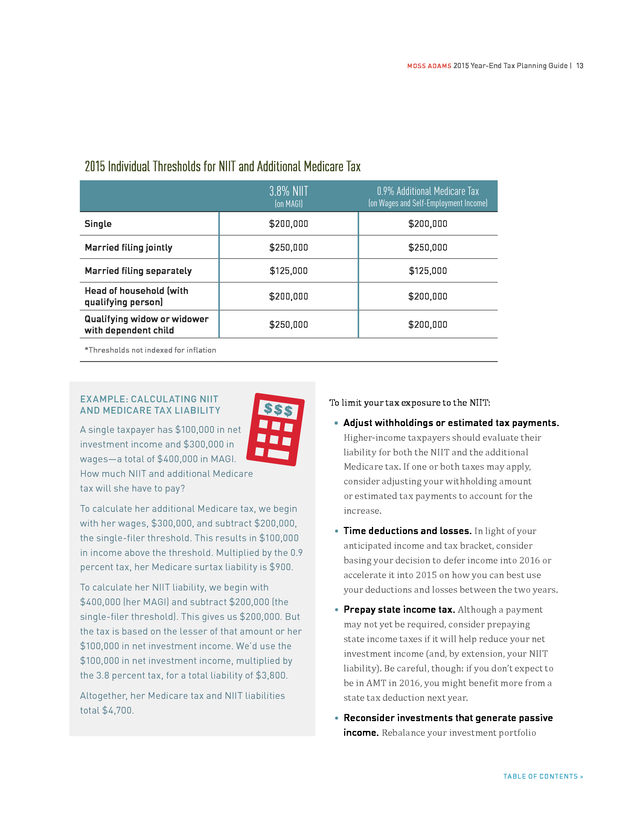

13) MOSS ADAMS 2015 Year-End Tax Planning Guide | 13 2015 Individual Thresholds for NIIT and Additional Medicare Tax 3.8% NIIT 0.9% Additional Medicare Tax (on MAGI) (on Wages and Self-Employment Income) Single $200,000 $200,000 Married filing jointly $250,000 $250,000 Married filing separately $125,000 $125,000 Head of household (with qualifying person) $200,000 $200,000 Qualifying widow or widower with dependent child $250,000 $200,000 *Thresholds not indexed for inflation EX AMPLE: CALCULATING NIIT AND MEDICARE TA X LIABILITY A single taxpayer has $100,000 in net investment income and $300,000 in wages—a total of $400,000 in MAGI. How much NIIT and additional Medicare tax will she have to pay? To calculate her additional Medicare tax, we begin with her wages, $300,000, and subtract $200,000, the single-filer threshold. This results in $100,000 in income above the threshold. Multiplied by the 0.9 percent tax, her Medicare surtax liability is $900. To calculate her NIIT liability, we begin with $400,000 (her MAGI) and subtract $200,000 (the single-filer threshold). This gives us $200,000. But the tax is based on the lesser of that amount or her $100,000 in net investment income. We’d use the $100,000 in net investment income, multiplied by the 3.8 percent tax, for a total liability of $3,800. Altogether, her Medicare tax and NIIT liabilities total $4,700. To limit your tax exposure to the NIIT: • Adjust withholdings or estimated tax payments. Higher-income taxpayers should evaluate their liability for both the NIIT and the additional Medicare tax. If one or both taxes may apply, consider adjusting your withholding amount or estimated tax payments to account for the increase. • Time deductions and losses. In light of your anticipated income and tax bracket, consider basing your decision to defer income into 2016 or accelerate it into 2015 on how you can best use your deductions and losses between the two years. • Prepay state income tax. Although a payment may not yet be required, consider prepaying state income taxes if it will help reduce your net investment income (and, by extension, your NIIT liability). Be careful, though: if you don’t expect to be in AMT in 2016, you might benefit more from a state tax deduction next year. • Reconsider investments that generate passive income. Rebalance your investment portfolio TABLE OF CONTENTS >

14) MOSS ADAMS 2015 Year-End Tax Planning Guide | 14 to include municipal bond investments, growth- oriented stocks that pay out lower dividends, and investments that produce income sheltered by depreciation or depletion (such as investments in real estate, energy, and natural resources). • Maximize your retirement contributions. Money you put into qualified retirement plans reduces your MAGI, which can reduce your NIIT liability. Note that distributions from retirement plans— such as individual retirement accounts (IRAs) or 401(k)s—aren’t subject to the NIIT. • Use like-kind exchanges. These kinds of transactions in place of cash can defer triggering taxable gains in rental or business real estate. • Use the installment method. Selling qualified assets in this manner will spread out gains, preventing you from triggering an NIIT or Medicare tax liability in any one tax year. • Revisit activity participation levels. How your income-generating activities are classified (as active or passive) and grouped with other activities can determine whether they’re subject to the NIIT. Look into ways you can materially participate in a trade or business in which you haven’t previously to reduce your NIIT exposure. If this is your first year paying the NIIT, talk with your tax advisor about the possibility of regrouping your activities. • Gift income-producing assets to children. While this won’t allow you to avoid the “kiddie tax” on your children’s income, your child may avoid paying the tax on up to $200,000 of net investment income. • Distribute trust income. As a trustee, consider whether net investment income left in the trust will be subject to the NIIT. If so, and if the trust document allows it, consider whether it would be better to distribute the income to beneficiaries with a MAGI below the applicable threshold such that beneficiaries won’t be subject to the NIIT. • Incorporate as an S corporation. Business owners with self-employment income on their individual income tax returns might want to consider incorporating and electing to be taxed as an S corporation. While you’d need to take a salary for the value of your service to the business, pass-through income from an S corporation that conducts active trade or business isn’t considered net investment income, and owners can take distributions of previously taxed profits that aren’t subject to tax. Furthermore, business owners conducting business using a single-member LLC can elect to be taxed as an S corporation and receive this same tax treatment. There are, however, significant federal and state tax and nontax issues to consider when changing from one form of entity to another, so review any such change carefully with your Moss Adams advisor. Real Estate Holdings With real estate markets recovering across the country and prices on the rise, opportunities to save related tax dollars are critical: • Take advantage of energy incentives. Through December 31, 2016, the Residential Energy Efficient Property Credit is available to taxpayers that install certain energy-efficient property, such as photovoltaic panels and solar water heaters. The credit can be used to offset both regular tax and AMT, and any unused credit can be carried forward to future years. • Make a Section 1031 exchange. Consider using a like-kind exchange (commonly referred to as a 1031 exchange) to sell a property, reinvest the proceeds in a new property, and postpone paying tax on the gain. Consult with your Moss Adams advisor prior to entering into a 1031 exchange TABLE OF CONTENTS >

15) MOSS ADAMS 2015 Year-End Tax Planning Guide | 15 to evaluate whether the property meets the IRS requirements. In addition, consider state and international tax ramifications: »» State considerations. Most states generally conform to the federal tax code with regard to like-kind exchanges; however, many have their own specific rules. Some states require you to buy a replacement property in the same state where the relinquished property was located. Others have their own rules for calculating the amount of deferred gain or specific provisions regarding the type or use of the property involved in the exchange. You’ll also want to consider if there’s any withholding tax at the state level as well as special reporting with the state income tax return in the year of the exchange. »» International considerations. Consult with your advisors before entering into a cross-border 1031 exchange. Some countries, including Canada, don’t recognize like-kind exchanges. This can result in a mismatch for foreign tax credit purposes. If, for example, a Canadian resident owns a US investment property that he or she exchanges for another US property, this is most likely a taxable transaction for Canadian purposes. As a result, deferring the US tax produces an unfavorable result because there isn’t any foreign tax credit to offset the Canadian tax. Tax Issues for Same-Sex Couples With the Supreme Court’s landmark decision this year on same-sex marriage—Obergefell v. Hodges in June 2015—there’s finally clarification on status of samesex married couples across the United States. The 2013 Supreme Court decision legalized all same-sex marriages at the federal level, and the 2015 decision overturned the remaining state and local bans on same-sex marriage, bringing marriage equality to all 50 states. Accompanying this decision are several tax and estate planning opportunities and issues same-sex couples should consider: • Consider amending prior tax returns. Examine whether amending your federal or state income tax returns or employment tax returns would provide any material economic benefit. Since the 2013 ruling, same-sex couples have been allowed to file married-filing-jointly returns for federal tax purposes, but states that didn’t previously allow same-sex couples to marry required couples to file separate state tax returns. Consult with your tax advisors to see whether there’s any tax benefit to amending previous-year federal or state income or employment tax returns. • Plan for the “marriage penalty.” If you’re planning on marriage in 2016, remember to consider the so-called marriage penalty in your tax planning process. The marriage penalty is common when both spouses earn similar incomes and file a joint tax return, which causes them to become subject to a higher tax rate than if they had remained two singly filing taxpayers. • Look into portability. Though there’s the potential you’ll pay higher income taxes as a married couple, same-sex married couples can now take advantage of the tremendous benefits of the portability provision under federal estate tax law. Under this provision, the unused portion of one spouse’s estate tax lifetime exclusion amount can be transferred to the surviving spouse. Consult with an estate planning attorney and update your estate documents to include this and other current estate and gift tax provisions. • Take the opportunity to split gifts. Newlywed spouses now have an opportunity to split gifts. Gift splitting allows the married couple to gift another person up to $28,000 per year (rather than $14,000) before they’re subject to the gift tax and TABLE OF CONTENTS >

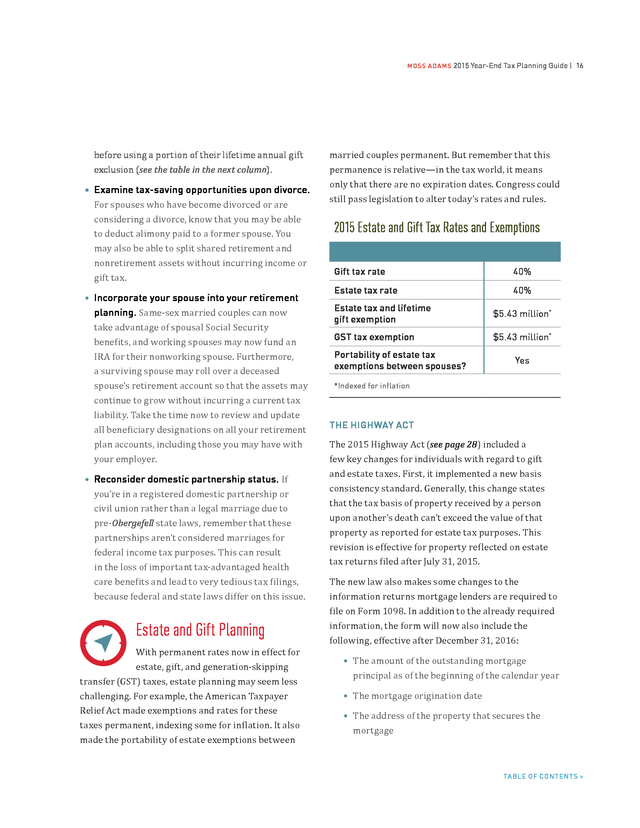

16) MOSS ADAMS 2015 Year-End Tax Planning Guide | 16 before using a portion of their lifetime annual gift exclusion (see the table in the next column). • Examine tax-saving opportunities upon divorce. For spouses who have become divorced or are considering a divorce, know that you may be able to deduct alimony paid to a former spouse. You may also be able to split shared retirement and nonretirement assets without incurring income or gift tax. • Incorporate your spouse into your retirement planning. Same-sex married couples can now take advantage of spousal Social Security benefits, and working spouses may now fund an IRA for their nonworking spouse. Furthermore, a surviving spouse may roll over a deceased spouse’s retirement account so that the assets may continue to grow without incurring a current tax liability. Take the time now to review and update all beneficiary designations on all your retirement plan accounts, including those you may have with your employer. • Reconsider domestic partnership status. If you’re in a registered domestic partnership or civil union rather than a legal marriage due to pre-Obergefell state laws, remember that these partnerships aren’t considered marriages for federal income tax purposes. This can result in the loss of important tax-advantaged health care benefits and lead to very tedious tax filings, because federal and state laws differ on this issue. Estate and Gift Planning With permanent rates now in effect for estate, gift, and generation-skipping transfer (GST) taxes, estate planning may seem less challenging. For example, the American Taxpayer Relief Act made exemptions and rates for these taxes permanent, indexing some for inflation. It also made the portability of estate exemptions between married couples permanent. But remember that this permanence is relative—in the tax world, it means only that there are no expiration dates. Congress could still pass legislation to alter today’s rates and rules. 2015 Estate and Gift Tax Rates and Exemptions Gift tax rate 40% Estate tax rate 40% Estate tax and lifetime gift exemption $5.43 million* GST tax exemption $5.43 million* Portability of estate tax exemptions between spouses? Yes *Indexed for inflation The 2015 Highway Act (see page 28) included a THE HIGHWAY ACT few key changes for individuals with regard to gift and estate taxes. First, it implemented a new basis consistency standard. Generally, this change states that the tax basis of property received by a person upon another’s death can’t exceed the value of that property as reported for estate tax purposes. This revision is effective for property reflected on estate tax returns filed after July 31, 2015. The new law also makes some changes to the information returns mortgage lenders are required to file on Form 1098. In addition to the already required information, the form will now also include the following, effective after December 31, 2016: • The amount of the outstanding mortgage principal as of the beginning of the calendar year • The mortgage origination date • The address of the property that secures the mortgage TABLE OF CONTENTS >

17) MOSS ADAMS 2015 Year-End Tax Planning Guide | 17 In 2015, the amount you can give during your lifetime LIFETIME GIFTS without incurring any gift tax has increased slightly and is currently set at $5.43 million (with an annual exclusion of $14,000 per recipient). This amount will be indexed for inflation annually. The gift tax rate on gifts greater than $5.43 million is 40 percent. If you plan to give, consider the following methods for reducing your tax exposure: • Take full advantage of the $14,000-per- recipient annual exclusion. Carefully consider your personal cash flow needs and long-term estate planning goals when you plan your gifts. Remember that your spouse can also gift $14,000 per recipient. • Plan the timing and type of gifts. When considering lifetime gifts above the annual exclusion, pay close attention to planning. Should the gifts be in cash or property? Outright or in trust? Should you give the entire asset now, or should it be given over time? How should the transfers be completed? And how can your family best utilize the step-up in asset basis for your estate? Work with your Moss Adams advisor to chart a tax-efficient course of action for your individual needs. • Mind state inheritance tax issues. Many states have an inheritance tax of their own, and the exemption amount is often much less than the federal amount ($5.43 million). This could create a situation where you might not owe federal estate tax but do owe it to the state you live in, so plan with an eye toward state as well as federal tax issues. LOW INTEREST RATE AND VALUATION OPPORTUNITIES • Refinance family loans. Applicable federal rates (AFRs)—which are the minimum interest rates that must be charged for bona fide loans between related parties—remain at generally historic lows. As such, it may be possible to refinance loans between family members or with a closely held business, significantly reducing interest payments. • Transfer wealth through trusts and leverage. The $5.43 million gift tax exemption, combined with historically low AFRs, creates an opportunity to transfer large amounts of wealth to your heirs through the use of leverage and certain types of trusts. Because these structures are complex, consult with your Moss Adams advisor as well as your estate attorney to determine how and whether you could benefit from this type of planning. • Transfer assets before they rise in value. If you’re holding any assets you believe will increase in value quickly, consider making a lifetime gift to (or a lifetime sale for) your beneficiaries now, before the values jump up significantly. Your Moss Adams advisor can evaluate your assets and help you determine whether this strategy makes sense for your individual situation. • Contribute property to a family-controlled GIFTING AND TRUST ENTITY STRUCTURES entity. A family limited partnership (FLP) is the preferred vehicle for this tax-saving technique. It provides the senior member continued control of the assets held in the FLP while gifting a portion to the next generation. The value of the portion gifted to the next generation is generally discounted from the fair market value. The discount can vary from as low as 5 percent to as high as 50 percent. Both value and discount are determined by an appraisal. TABLE OF CONTENTS >

18) MOSS ADAMS 2015 Year-End Tax Planning Guide | 18 Discounting an interest in the FLP allows the senior member to gift more without incurring a tax, and it freezes the asset value. Note that the IRS has generally frowned upon discounts on gifted entities, but it hasn’t had much luck in limiting this technique’s use. The tax code provides the US Treasury—which runs the IRS— with discretion to revise its interpretation of the tax code through regulations. There’s been talk for a while about the Treasury creating regulations to limit discounting in this type of transaction, and this talk may be turning into a reality—maybe even by the end of the year. If the Treasury does issue such regulations, this type of transaction will become a • Form a grantor-retained annuity trust (GRAT). In this technique, a grantor gives an asset to a GRAT. In turn, the GRAT pays the grantor an annuity stream based on the current value of the asset. The annuity is a fixed amount determined after the value of the assets is set. Usually transfer has no gift tax consequences because the annuity stream is the present value of the asset transferred. The GRAT exists while the annuity payments are being made—as little as two years up to 10 or more—then terminates, at which point the GRAT’s beneficiary ( a trust or individual) receives the remaining asset. thing of the past. GRATs: Pros and Cons PROS CONS • The income from the asset being transferred is generally recognized on the grantor’s income tax return, which increases the estate benefit by depleting the grantor’s estate rather than the beneficiaries’. • Grantors pay income tax on the income from the asset transferred to the GRAT. This could deplete a grantor’s estate faster than expected without a proper analysis of the transaction. • The annuity payment is based on current Section 7520 rates, which could be as little as 2 percent. • The GRAT must have enough cash to make the annuity payments, which usually means either transferring an asset that produces heavy cash flow or the GRAT borrowing money from an unrelated party. • A GRAT can be set up without gift tax consequences, helpful to those who wish to exceed the $5.43 million lifetime exemption. • GRATs can be created in such a way that they reduce the risk of underperforming assets that would otherwise negate the GRAT’s benefits. • If the grantor passes away during the life of the GRAT, a portion of the value of the annuity is included in the estate. • President Obama has been trying to limit the use of GRATs for years, and though he’s been unsuccessful with the Senate so far, this will likely be a big push during his final year in office. TABLE OF CONTENTS >

19) MOSS ADAMS 2015 Year-End Tax Planning Guide | 19 DEVELOPING OR UPDATING YOUR ESTATE PLAN In addition to the specific estate and gift planning opportunities previously covered in this section, remember that the end of the year is an ideal time to revisit your plan as a whole (or create one, if you don’t already have one). Here are a few of the items you should be sure to cover: • Understand and revisit your goals. Work with your Moss Adams advisor as well as your estate attorney to make sure your plan addresses your cash flow, business, and family needs as well as your charitable wishes. • Check through your documentation. Confirm that your assets are properly titled and the beneficiary designations are correct. • Plan for transition. If you’re one of the many business owners who will sell your business to a new owner in the next five to 10 years, make sure your estate plan is closely aligned with your business and personal goals. A smooth transition of ownership interests will also help protect your wealth after the sale of your business. • Understand how federal and state estate tax »» As of 2015 every estate will have a federal exemption of $5.43 million per spouse and a top tax rate of 40 percent, including full step-up in basis for most estate assets. laws will affect you. »» Portability, the ability to use a deceased spouse’s unused estate federal tax exemption, remains a viable planning technique. »» Many states have their own estate tax, and in many cases the exemption amounts are lower than the federal amounts. Don’t overlook gifting and estate planning opportunities as they relate to applicable state inheritance tax. Charitable Giving Making a charitable contribution may entitle you to an income tax deduction in the year you make the gift. Most deductible contributions are those made to US organizations described in Section 501(c) (3) of the Internal Revenue Code. This includes not-for-profit entities organized and operated for charitable, scientific, educational, religious, and other purposes. Contributions to nonqualifying charitable organizations aren’t deductible. A few tax-saving opportunities to consider when engaging in charitable activities: • Examine any volunteering activities and expenses. Unreimbursed out-of-pocket expenses incurred in rendering volunteer services may be deductible as direct payments to a charitable organization, so keep good records of these expenditures. If you use your vehicle for charitable purposes, you can deduct the mileage at $0.14 per mile or actual cost of gas and oil. You can deduct tolls and parking fees regardless of whether you use the standard mileage or actual expense methods. • Gift appreciated or depreciated property. »» Giving a charity appreciated capital gain property that you’ve held for more than one year instead of cash will get you a deduction for the fair market value of the assets. Additionally, you’ll avoid paying tax, including the NIIT (see page 12), on the capital gain. »» When you use investment assets that have declined in value to make charitable contributions, sell the assets first, then donate the cash proceeds to charity. That way, you’ll get the benefit of the capital loss in addition to the charitable deduction. TABLE OF CONTENTS >

20) MOSS ADAMS 2015 Year-End Tax Planning Guide | 20 • Plan the timing of larger charitable gifts. Around year-end, take the opportunity to consider whether making large charitable contributions in 2015 or 2016 will provide the greater benefit from a tax perspective. • Account for charitable deductions in AMT calculations. Although state, local, and foreign taxes aren’t deductible in determining taxable AMT income, qualified charitable contributions are, subject to certain conditions. Work with your Moss Adams advisor to determine which itemized deduction would be more beneficial for you. • Use credit cards and checks to squeeze in final 2015 deductions. You can make year-end charitable contributions using your credit card. The gift must be processed and charged to your card by December 31 to be deductible on your 2015 tax return. Checks to charities must be written and postmarked by December 31 for a 2015 deduction. • Choose a recipient later using donor-advised funds. If you want to take a large charitable deduction in 2015 but haven’t decided on a charity (or charities) to receive your gift, consider making a charitable contribution by year-end to a donoradvised fund. This will allow you to use the large charitable deduction in the current year, but you’ll still be able to give the money to charities over time. If the charitable contribution is large enough, you may also want to consider establishing a private foundation. Discuss the costs and benefits with your Moss Adams advisor before doing so. CHARITABLE GIVING AS PART OF YOUR OVERALL ESTATE PLAN By incorporating your charitable contribution planning into your long-term estate plan strategy, you can help increase cash flow for yourself and your heirs while achieving your charitable goals. • Consider setting up a charitable remainder trust. If you plan to make sizable donations, this will allow you to take the deduction when you fund the trust; the remaining assets will be passed to charitable organizations at the end of the trust term. Properly structured and administered, the trust can also accumulate greater assets without incurring a tax burden, since the trust is taxexempt. • Designate charitable organizations as retirement account beneficiaries. In doing so, assets held in accounts such as 401(k)s and IRAs fund your charitable bequests while minimizing income and transfer tax consequences. • Keep tabs on complexity. Direct contributions to qualified organizations, donor-advised funds, and charitable trusts each come with their own complexities and costs. As a donor, balance the size of the charitable contribution with the complexity of the gifting vehicle. »» Direct contributions are the least complex and have the lowest maintenance cost as a one-time event. »» Charitable trusts are the most complex of the three options and can have the highest maintenance cost due to the longevity of the entity. TABLE OF CONTENTS >

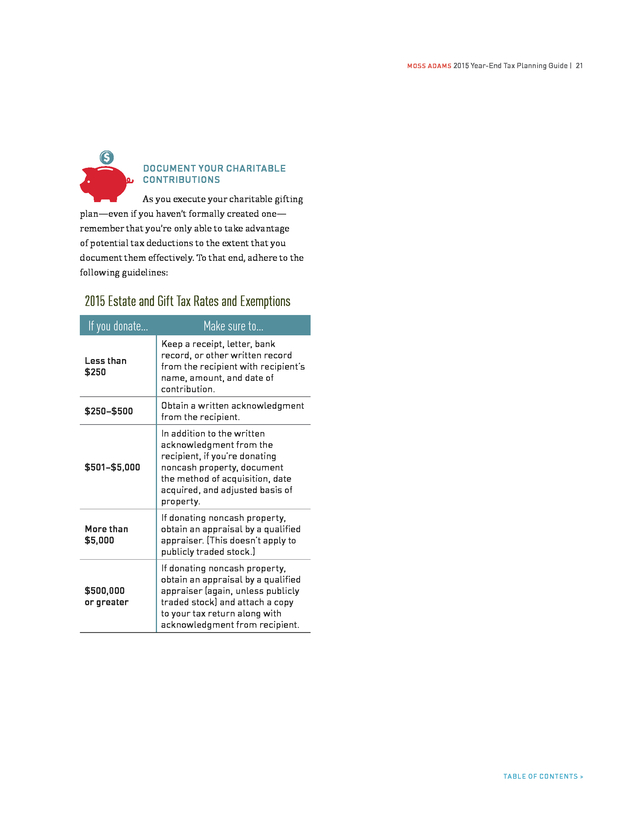

21) MOSS ADAMS 2015 Year-End Tax Planning Guide | 21 DOCUMENT YOUR CHARITABLE CONTRIBUTIONS As you execute your charitable gifting plan—even if you haven’t formally created one— remember that you’re only able to take advantage of potential tax deductions to the extent that you document them effectively. To that end, adhere to the following guidelines: 2015 Estate and Gift Tax Rates and Exemptions If you donate… Make sure to… Less than $250 Keep a receipt, letter, bank record, or other written record from the recipient with recipient’s name, amount, and date of contribution. $250–$500 Obtain a written acknowledgment from the recipient. $501–$5,000 In addition to the written acknowledgment from the recipient, if you’re donating noncash property, document the method of acquisition, date acquired, and adjusted basis of property. More than $5,000 If donating noncash property, obtain an appraisal by a qualified appraiser. (This doesn’t apply to publicly traded stock.) $500,000 or greater If donating noncash property, obtain an appraisal by a qualified appraiser (again, unless publicly traded stock) and attach a copy to your tax return along with acknowledgment from recipient. TABLE OF CONTENTS >

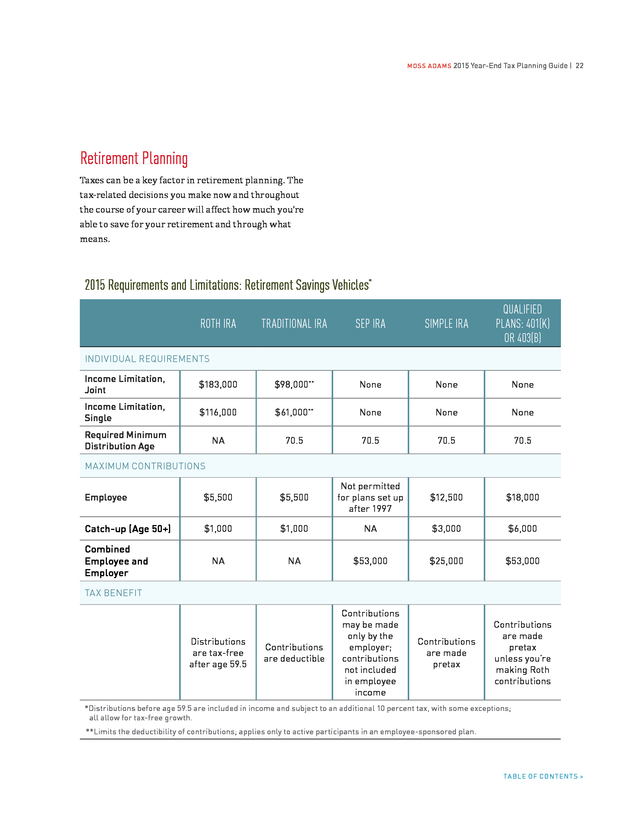

22) MOSS ADAMS 2015 Year-End Tax Planning Guide | 22 Retirement Planning Taxes can be a key factor in retirement planning. The tax-related decisions you make now and throughout the course of your career will affect how much you’re able to save for your retirement and through what means. 2015 Requirements and Limitations: Retirement Savings Vehicles* ROTH IRA TRADITIONAL IRA SEP IRA SIMPLE IRA QUALIFIED PLANS: 401(K) OR 403(B) INDIVIDUAL REQUIREMENTS Income Limitation, Joint $183,000 $98,000** None None None Income Limitation, Single $116,000 $61,000** None None None Required Minimum Distribution Age NA 70.5 70.5 70.5 70.5 Employee $5,500 $5,500 Not permitted for plans set up after 1997 $12,500 $18,000 Catch-up (Age 50+) $1,000 $1,000 NA $3,000 $6,000 NA NA $53,000 $25,000 $53,000 Contributions are deductible Contributions may be made only by the employer; contributions not included in employee income Contributions are made pretax Contributions are made pretax unless you’re making Roth contributions MAXIMUM CONTRIBUTIONS Combined Employee and Employer TAX BENEFIT Distributions are tax-free after age 59.5 *Distributions before age 59.5 are included in income and subject to an additional 10 percent tax, with some exceptions; all allow for tax-free growth. **Limits the deductibility of contributions; applies only to active participants in an employee-sponsored plan. TABLE OF CONTENTS >

23) MOSS ADAMS 2015 Year-End Tax Planning Guide | 23 IS YOUR IRA PROTECTED IN BANKRUPTCY? Following a 2014 US Supreme Court decision, inherited IRAs no longer have the same level of bankruptcy protection as some other retirement assets. If you’re concerned about keeping your longsaved money away from potential future creditors— which can include creditors of a spouse, children, or other beneficiaries—after you’re gone, consult with your Moss Adams advisor and your attorney. • Establish certain plans before year-end. Keogh plans, 401(k) plans, and certain others allow larger tax deductions, but they must be established by year-end—even though contributions don’t need to be made by that time. If you’re considering options for a company retirement plan, be sure to have it in place before December 31. • Weigh the benefits of a Roth IRA. Any taxpayer can now convert a traditional IRA to a Roth IRA, regardless of income. Certain qualified plans may allow for an “inside the plan” conversion, which generate earned income. Those earnings can be contributed or funds could be gifted into the IRA accounts. • Contribute to a myRA account. Finalized in December 2014, this is a no-risk, Treasury- backed Roth IRA investment account intended for beginner retirement savers who don’t otherwise have access to an employer-sponsored plan. Some of the details are as follows: »» There’s no cost to employers or to participants, and contributions are made via direct deposit. You can sign up at www.myRA.gov. »» The same income and contribution limitations that apply to a Roth IRA apply to a myRA: For 2015, annual income generally must be less than $131,000 for individuals and $193,000 for married couples filing jointly. Annual contributions are limited to $5,500 ($6,500 for individuals over 50 years of age). »» Participants are limited to an account balance of $15,000, after which they must transfer the account to a private-sector Roth IRA. should also be considered where appropriate. Discuss this strategy and the accompanying tax consequences with your Moss Adams advisor. Wealth Management Effective January 1, 2015, the once-a-year limit on IRA rollovers that aren’t direct custodian-tocustodian transfers will apply to all your IRAs in preserving and generating investment returns, growing your assets, creating sustainable income, and achieving financial security. The decisions you • Watch for penalties with multiple IRA rollovers. in aggregate rather than to each one separately. Consult with your Moss Adams advisor to make sure any rollovers comply with the new aggregate rules and don’t generate an unnecessary tax liability, interest, or penalties. • Employ children to jump-start retirement savings. If a child has earned income, there are strategies he or she can use to contribute to a traditional or Roth IRA. Where practical, consider employing children in the family business to While tax planning shouldn’t be the sole driver of investment decisions, it can play an important role make today and throughout the course of your career can affect your short- and long-term investments as well as your taxes. Seek advice from both a tax and investment perspective so you can rest assured, knowing the two are aligned with your wealth management goals. • Account for the impact of state taxes. When INVESTMENT MANAGEMENT AND STRATEGY selecting municipal bonds for the federal tax- TABLE OF CONTENTS >

24) MOSS ADAMS 2015 Year-End Tax Planning Guide | 24 free interest income, consider the impact of state income taxes as well. • Consider realizing losses. Work with your investment advisor to manage net capital gains and take advantage of any unrealized capital losses that may be in your account (tax-loss harvesting). • Reevaluate and rebalance. Given recent equity market performance, review your investment strategy to determine whether your asset allocations remain consistent with your personal goals and if it’s time to rebalance your portfolio. • Evaluate the impact of the NIIT. Reevaluate tax-exempt yields versus taxable yields in light of current market conditions and the 3.8 percent tax (see page 12). • Create or update your personal financial plan. PERSONAL FINANCIAL PLANNING For those without a plan, take the time to set clear short- and long-term goals, and begin to monitor your progress toward those goals. If you do have a plan, ensure you’re still on track. The strong market performance and economic recovery of the past few years are good reasons to make updates and mark your progress. • Reevaluate your needs. Update your policies INSURANCE to ensure they’re still in accordance with your current needs, transfer goals, and liquidity concerns. Pay particular attention to policy type, coverage amounts, ownership, and beneficiary designations. • Check in on policy performance. Review your existing insurance policies, including annuities, to confirm they’re performing as expected and operating efficiently. • Review employer-owned policies. If you purchased a new employer-owned life insurance policy, confirm that the required formalities are being followed. If not, the proceeds could become taxable income when received, increasing the corresponding tax liability. International Considerations Understanding the tax implications of cross-border transactions and investments is even more critical today than ever before. For example, US taxpayers living outside the United States need to be alert to special issues in estate planning, and US citizens with noncitizen spouses have issues of their own to address. Increasing numbers of Americans live, work, and—especially—invest abroad, activities that may create a host of filing requirements and potential traps for the unwary. Significant and frequently negative tax issues may also be created when individuals immigrate to or expatriate from the United States. The following considerations may help you reduce your tax burden and reduce your risk: • Consult with your advisor regarding any foreign mutual fund investments. Virtually all foreign mutual funds are considered to be passive foreign investment companies (PFICs) for US income tax purposes. Investing in a PFIC may essentially double your tax burden related to gains or income from the investment compared to a non-PFIC investment unless you make certain elections; in fact, in some situations it creates significant tax liabilities when no economic gain has actually been realized. Furthermore, a US person who owns an interest in a PFIC is required annually to file Form 8621 to report information regarding the investment. A separate form must be filed for each such investment owned. However, careful planning TABLE OF CONTENTS >

25) MOSS ADAMS 2015 Year-End Tax Planning Guide | 25 and timely tax elections may allow you to reduce the US tax on investments in foreign mutual funds. Discuss with your advisor whether your foreign life insurance or foreign pension may also invest in foreign mutual funds, because PFIC rules may also apply. • Review tax amnesty program options. The IRS has recently made several changes to the Offshore Voluntary Disclosure Program (OVDP), the Streamlined Foreign Offshore Procedures (SFOP), and the Streamlined Domestic Offshore Procedures (SDOP). These programs are designed for US taxpayers who have unreported foreign income for prior years or who haven’t submitted all the required disclosure forms to the IRS. The OVDP essentially offers delinquent taxpayers an alternative to potential criminal prosecution and the effective confiscation of the unreported foreign assets, while the SFOP and SDOP may greatly reduce the penalties of what’s termed “noncompliance without malice.” We strongly recommend that you work with your tax advisor to conduct a careful review of each program in light of your specific circumstances prior to entering into one of these three programs. • File a US tax return, even if you’re overseas. Unlike most nations, the US requires citizens residing outside the United States to file annual US income tax returns and to pay tax on their worldwide income. Frequently, US individuals living in countries with a higher tax rate will owe little or no net US income tax, because they may be able to claim a foreign tax credit or the foreignearned income exclusion. However, in order to claim the credit or the exclusion the United States, the person is still required to file a US tax return. Note that the foreign tax credit doesn’t offset the NIIT (see page 12), so US citizens living overseas should discuss their investment alternatives with their advisor. Health Care Reform A number of Affordable Care Act provisions in addition to the NIIT and Medicare surtax will impact individuals and families that don’t receive health insurance under an employer’s plan. • Gather documentation to substantiate your 2015 coverage. Starting this year, insurance companies are required to report the coverage provided to health insurance policyholders on the new Form 1095-B. Employers will report whether they offered minimum essential coverage to their employees on Form 1095-C. Employers with self-insured health plans may choose to report both insurance offered and the coverage actually provided on a single Form 1095-C by filling out Part III of that form. You should receive these forms for the 2015 tax year by January 31, 2016, and you’ll need them to report minimum essential coverage on 2015 individual income tax returns. • Renew or purchase your 2016 coverage. Marketplace coverage for 2015 ends on December 31, 2015. You can either renew your existing health plan or choose a new plan via the marketplace during the 2015 open enrollment period, which opened November 1, 2015, and ends January 31, 2016. Coverage can start as soon as January 1, 2016, as long as you complete your enrollment by December 15, 2015. Here’s a refresher on a few of the key points of the individual shared-responsibility provision: »» All US citizens and legal residents are required to have qualifying minimum essential health coverage as of January 1, 2014. You and your family must have health care coverage, have an exemption from coverage, or make a penalty payment when you file your 2015 tax return in 2016. TABLE OF CONTENTS >

26) MOSS ADAMS 2015 Year-End Tax Planning Guide | 26 »» If you decide to forgo coverage, the 2015 penalty for not obtaining qualifying health coverage is the greater of $325 per adult ($162.50 per child) or 2 percent of household income. In 2016 the penalty increases to the greater of $695 per adult ($347.50 per child) or 2.5 percent of household income. The penalty will be indexed for inflation after 2016. »» The maximum penalty for a family is three times the penalty of an adult individual. The penalty for dependents under age 18 is half the penalty of an adult individual. »» There are some exemptions from the individual shared responsibility provision, including certain situations where coverage is unaffordable or you are without coverage for a short period of time. Ask your Moss Adams advisor for more information on whether the exemption may apply to your particular situation. TABLE OF CONTENTS >

27) Tax Planning for Business Owners and Businesses MOSS ADAMS 2015 Year-End Tax Planning Guide | 27 Tax planning for business owners often requires consideration of the tax consequences to the owner as an individual taxpayer and vice versa, so be sure to review the previous section on tax planning for individuals (see page 6). Tax Planning for Business Owners and Businesses Highlight: Self-Rental Planning 28 Employee Benefits 34 Depreciable Real Estate 29 Entity Structure 34 Sales and Acquisitions 37 and Pitfalls Highlight: The Highway Act and Business Equipment Business Credits Tangible Property Regulations Health Care Reform International Tax The Foreign Account Tax Compliance Act 28 30 31 32 33 Benefits for Same-Sex Married Couples Ownership Transition Exit Planning 34 35 36 33 TABLE OF CONTENTS >

28) MOSS ADAMS 2015 Year-End Tax Planning Guide | 28 Highlight: Self-Rental Planning and Pitfalls Business owners commonly acquire real estate that they then lease to their businesses. These function as investment assets, and they’re often owned by a legal entity (such as an LLC) separate from the business for a variety of legal, financial, tax, and personal reasons. One common benefit of rental real estate ownership is the tax losses they generate as a result of depreciation, mortgage interest expense, real estate taxes, and other property maintenance expenses—particularly in the early years of ownership. Yet despite the routine nature of these arrangements, it comes as a surprise to many that these tax losses may not be immediately deductible against their other sources of income, such as wages, capital gains, or business income. By default, rental real estate income and losses are This situation was the topic of a recent court case (Tax Court Memo 2015-76) in which the taxpayer owned an S corporation and a C corporation. The S corporation owned real property, which it leased to the C corporation. The C corporation was an operating business in which the taxpayer materially participated. The taxpayer also owned other passive rental properties and business entities. In the years at issue, the S corporation generated net taxable income, which the taxpayer used to offset losses from other passive activities. The IRS challenged this treatment under the self-rental rules, claiming that the taxpayer couldn’t deduct other passive losses against the S corporation’s rental income because the self-rental rules recharacterized the S corporation’s rental income as nonpassive. The Tax Court upheld the IRS’s position and reaffirmed that the self-rental rules apply “passive,” and passive losses are deductible only even to activities owned by taxpayers through legal passive income, such as that from a business he or and the issue is only exacerbated for taxpayers who against other sources of passive income. For example, a taxpayer whose rental property generates a passive loss would generally be able to deduct it only against she doesn’t materially participate in or other passive rental income. The self-rental rules are one common exception to this rule. If a taxpayer rents property to a business that he or she owns (and materially participates in), the rental activity will be subject to the self-rental rules. This also applies if the taxpayer owns the property through a legal entity, such as an S corporation, LLC, or closely held C corporation. These self- rentals can impact whether income and losses are characterized as passive or nonpassive: When the self-rental rules apply and the activity generates net taxable income for the year, it’s treated as income from a nonpassive activity. But if it generates a net taxable loss for the year, it’s treated as a passive loss. This recharacterization of rental income can have unanticipated tax consequences for taxpayers who may otherwise expect to deduct a passive loss. entities. Given this common fact pattern, taxpayers often find themselves owing more tax than they anticipated, must also pay the NIIT (see page 12). The bottom line: When multiple businesses and rental properties are involved, be diligent in your tax planning, and consider the effect of self-rental and passive activity rules on the deductibility of your tax losses. Work with your advisor to execute proper planning, tax elections, and entity structuring to increase your tax deductions and reduce your overall tax obligations. Highlight: The Highway Act On July 31, 2015, President Obama signed a new law called the Surface Transportation and Veterans Health Care Choice Improvement Act of 2015, also known as the 2015 Highway Act. Although none of these changes are effective for the upcoming 2015 tax filing season, TABLE OF CONTENTS >

29) MOSS ADAMS 2015 Year-End Tax Planning Guide | 29 this summary will give you a good idea of what’s • Calendar-year C corporations will have a certain types of entities, allows extensions for foreign • The tax returns for trusts will have a five-and- The largest change is a restructuring of business • Tax returns for employee benefit plans filing coming down the road. This new law revises due dates for partnership and corporate tax returns, revises the extension rules for bank account reports (FBARs), sets a new basis consistency standard, and makes changes to mortgage information returns. entity tax return due dates, generally effective for business tax returns for tax years after December 31, 2015, which means that the due dates below will impact your 2016 tax returns (that is, the 2017 filing season): • Partnership tax returns will now be due the 15th day of the third month after the end of the tax year. (Under preexisting tax law, returns were due the 15th day of the fourth month.) This means if your partnership has a December 31 year-end, your tax return will be due March 15. • C corporation tax returns will be due by the 15th day of the fourth month after the end of the tax year. (Under preexisting tax law, these were due on the 15th day of the third month). This is to say that if your C corporation has a December 31 year-end, your tax return is due April 15. • For C corporations with fiscal years ending June 30, the change won’t go in effect until after December 31, 2025. Related to the revised due dates for certain tax returns, there have also been changes to the extension rules. These changes are effective for tax years beginning after December 31, 2015, which, again, affects your 2016 tax returns: • While the extended due date for partnership tax returns hasn’t changed (September 15), taxpayers will have a full six-month extension as opposed to the current five-month period. five-month extension, while C corporations with June 30 year-ends will have a seven-month extension period. a-half-month extension period, meaning the extended due date for trusts will be September 30. Form 5500 will have an extended due date of November 15, giving them an automatic threeand-a-half-month extension. • Tax returns for tax-exempt organizations will get an automatic six-month extension as opposed to the current three-month extension, so that the period ends November 15. Another important change is related to Financial Crime Enforcement Network (FinCEN) Form 114, Report of Foreign Bank and Financial Reports, effective for tax years beginning after December 31, 2015. This report has always been due on or before June 30 of the year immediately following the calendar year being reported, and it was never allowed an extension. That has now changed: under the Highway Act, the due date will be April 15, with a maximum sixmonth extension to October 15. These due dates are now consistent with the individual tax return filings. Depreciable Real Estate and Business Equipment Many of the tax breaks related to depreciable real estate and business equipment expired at the end of 2014, including the ability of certain real property to qualify for the Section 179 expense deduction and the 50 percent bonus depreciation provision for qualified assets acquired and placed in service during the year. As of October 1, 2015, these expired tax breaks haven’t been extended or otherwise renewed. While TABLE OF CONTENTS >

30) MOSS ADAMS 2015 Year-End Tax Planning Guide | 30 we anticipate these items will be extended, it isn’t a certainty. Visit www.mossadams.com/insights and click Subscribe to sign up for e-mail Alerts on this topic and others. Still, the following strategies are available in 2015 to help you potentially save on business taxes: • Perform a cost segregation study. Accelerate the cash flow benefit of depreciation deductions via a detailed review of the depreciable components of a building. Cost segregation studies, performed by an integrated team of accountants and engineers, result in the ability to take a large current-year tax deduction for depreciation by reclassifying longerlived property into shorter recovery periods. The tax savings can result in a dramatic cash flow increase. It’s particularly appropriate to do a cost segregation study on buildings purchased or inherited within the past five years. • Use the Section 179 depreciation deduction. The deduction for qualifying assets acquired in 2015 is subject to a $25,000 limit. It begins to phase out once total depreciable assets purchased during the year exceed $200,000, decreasing dollar-for-dollar above that threshold. • Take bonus depreciation on qualifying property. First-year bonus depreciation is available only for certain property with longer production periods placed in service during 2015. • Understand your state’s depreciation rules. Not all states conform to federal depreciation laws for Section 179 expenses or bonus depreciation, so make sure you understand the impact such a strategy at the federal level may have on your state tax liability. Business Credits A number of business tax credits and incentives are available in 2015 to help you reduce what you owe. In addition to those listed here, be sure to consider hiring and zone-based credits as well as those available at the state and local level. • Claim small-employer health insurance credits. Eligible small employers are allowed a credit for 50 percent of certain contributions made to purchase health insurance for their employees. Eligible employers are generally those with 10 or fewer full-time equivalent employees (FTEs) with wages of $25,000 or less that offer a qualified health plan (QHP) through a Small Business Health Options Program exchange. The credit amount begins to phase out for employers with either 11 FTEs or average annual employee wages of more than $25,000. The credit is phased out completely for employers with 25 or more FTEs or average annual employee wages of $50,000 or more. Certain small employers whose principal business is in an exception county in Washington or Wisconsin—which the Department of Health and Human Services advised will not have QHPs available—may qualify for an exception. • Take advantage of the employer-provided child care credit. Employers can claim a credit of up to $150,000 for supporting employee child care or child care resource and referral services. This provision has been extended permanently. • Explore research and development (R&D) tax credits. If your organization develops new or improved products or processes, it may be able to benefit from federal and state (where applicable) R&D tax credits. The R&D tax credit is a dollar-fordollar credit against taxes owed or paid. Although the federal credit expired at the end of 2014, it likely will be re-extended retroactive to January 1, 2015; after all, it has been extended 15 times TABLE OF CONTENTS >

31) MOSS ADAMS 2015 Year-End Tax Planning Guide | 31 since its inception in 1981. Most states’ credits are unaffected by the lapse at the federal level. Stay up to date on the status of the extension, recent law changes, and related court cases by joining our discussion group on LinkedIn: R&D Tax Credits Forum, facilitated by Moss Adams LLP. Tangible Property Regulations The final tangible property regulations— issued by the IRS in two installments in September 2013 and September 2014—are effective for tax years beginning on or after January 1, 2014. They apply to all taxpayers that acquire, produce, or improve tangible property. • Review your compliance with the new regulations. With the mandatory effective date already behind us, it’s imperative that business owners understand the impact of the regulations on their company and create an implementation and ongoing compliance plan as soon as possible to avoid filing-season surprises. Review your asset capitalization policies to see that they’re in compliance with the new regulations and consult with your Moss Adams advisor for help implementing necessary changes. WHAT SHOULD YOU CAPITALIZE VERSUS EXPENSE? Under the tangible property regulations, improvements to tangible property must generally be capitalized. A unit of property is said to have been improved when activities are performed after the property has been placed in service that result in the betterment, restoration, or adaptation of the unit of property to a new or different use. These three possibilities together are known as the BAR test. For buildings, a “unit of property” is either the building structure or one of nine specified building systems. If costs incurred aren’t required to be capitalized, they may be treated as deductible expenses. Depending on the specific facts and circumstances, the new regulations may lead to increased capitalization or, in some cases, increased deductions. Learn more and find related resources at www.mossadams.com/tpr. • Examine your eligibility for related safe harbors. Several safe harbors are available under the tangible property regulations. One of these applies to routine maintenance on building and nonbuilding property; another allows small taxpayers to deduct minor building repairs. For simplicity, you can also elect to capitalize repairs for tax purposes if you’re already capitalizing them for financial statements. To do so, you’ll need to attach an election statement to your return. • Review dispositions annually. Conduct an annual review of dispositions to see if you can take advantage of the new rule that allows taxpayers to elect a deduction of partially disposed assets. The election generally applies to assets that are disposed in the current year as a result of property improvements. For fiscal-year taxpayers that haven’t yet filed a 2014 return, the partial disposition election may be available for assets disposed in prior years as well. If you fall into one of these scenarios or are planning significant improvements in the future, consult with your Moss Adams advisor as soon as possible to evaluate whether you can take advantage of these deductions. • Put your capitalization policy in writing. Generally, you may follow your financial statement capitalization policy for purchases up to a specified de minimis amount (per invoice or item) if you’ve TABLE OF CONTENTS >