1) The Financially Unengaged

Reaching the 16% of Americans Who

Aren’t in Touch With Their Financial Standing

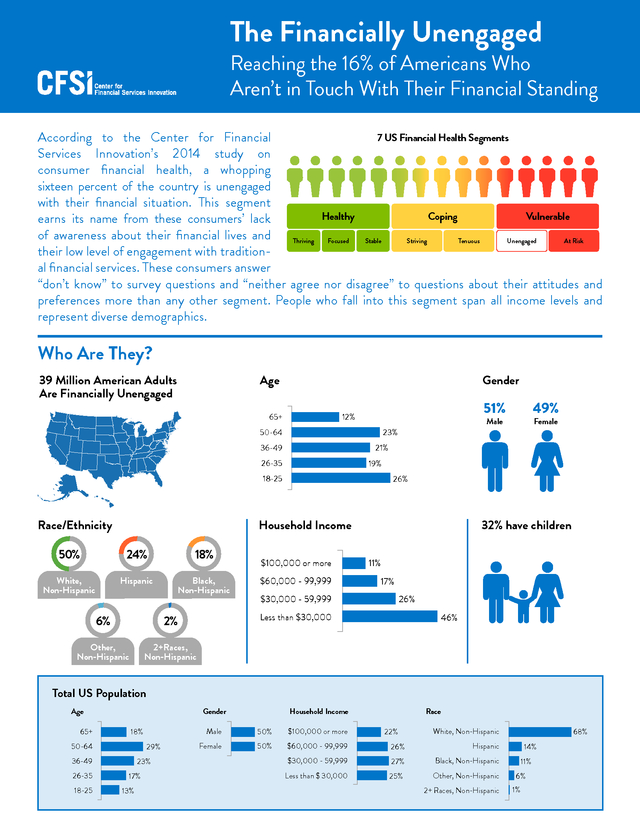

7 US Financial Health Segments

According to the Center for Financial

Services Innovation’s 2014 study on

consumer financial health, a whopping

sixteen percent of the country is unengaged

with their financial situation. This segment

Healthy

Coping

Vulnerable

earns its name from these consumers’ lack

of awareness about their financial lives and

Thriving

Focused

Stable

Striving

Tenuous

Unengaged

At Risk

their low level of engagement with traditional financial services. These consumers answer

“don’t know” to survey questions and “neither agree nor disagree” to questions about their attitudes and

preferences more than any other segment. People who fall into this segment span all income levels and

represent diverse demographics.

Who Are They?

39 Million American AdultsAdults Adults Age

39 MillionMillion American

39 American

Age

Are Financially Unengaged Unengaged

Are Financially Unengaged

Are Financially

Age

65+

65+

50-64

50-64

50-64

36-49

36-49

36-49

26-35

26-35

26-35

18-25

18-25

18-25

Race/Ethnicity

65+

12%

Gender

Gender

Gender

12%

19%

Male

23%

23%

23%

21%

51% 51% 51%

49% 49% 49%

12%

21%

19%

26%

26%

Household Income

50%

24%

18%

White,

Non-Hispanic

Hispanic

Black,

Non-Hispanic

6%

$60,000 - 99,999

32% have children

11%

17%

$30,000 - 59,999

26%

Less than $30,000

2%

Other,

Non-Hispanic

$100,000 or more

Female

21%

19%

26%

MaleFemale Female

Male

46%

2+Races,

Non-Hispanic

Total US Population

Age

65+

29%

36-49

18-25

23%

17%

13%

Race

Male

18%

50-64

26-35

Household Income

Gender

50%

$100,000 or more

Female

50%

$60,000 - 99,999

26%

Hispanic

$30,000 - 59,999

27%

Black, Non-Hispanic

Less than $ 30,000

25%

22%

White, Non-Hispanic

Other, Non-Hispanic

2+ Races, Non-Hispanic

68%

14%

11%

6%

1%

�

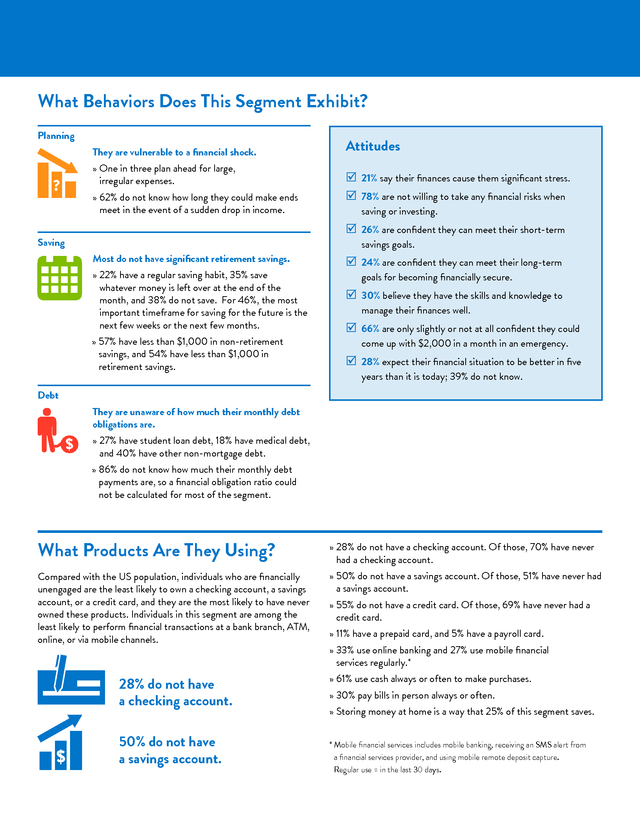

2) What Behaviors Does This Segment Exhibit?

Planning

They are vulnerable to a financial shock.

» � ne in three plan ahead for large,

O

irregular expenses.

?

» � 2% do not know how long they could make ends

6

meet in the event of a sudden drop in income.

Attitudes

þ �21% say their finances cause them significant stress.

�

þ �78% are not willing to take any financial risks when

�

saving or investing.

þ �26% are confident they can meet their short-term

�

Saving

Most do not have significant retirement savings.

» � 2% have a regular saving habit, 35% save

2

whatever money is left over at the end of the

month, and 38% do not save. For 46%, the most

important timeframe for saving for the future is the

next few weeks or the next few months.

» � 7% have less than $1,000 in non-retirement

5

savings, and 54% have less than $1,000 in

retirement savings.

savings goals.

þ �24% are confident they can meet their long-term

�

goals for becoming financially secure.

þ �30% believe they have the skills and knowledge to

�

manage their finances well.

þ �66% are only slightly or not at all confident they could

�

come up with $2,000 in a month in an emergency.

þ �28% expect their financial situation to be better in five

�

years than it is today; 39% do not know.

Debt

They are unaware of how much their monthly debt

obligations are.

$

» � 7% have student loan debt, 18% have medical debt,

2

and 40% have other non-mortgage debt.

» � 6% do not know how much their monthly debt

8

payments are, so a financial obligation ratio could

not be calculated for most of the segment.

What Products Are They Using?

» � 8% do not have a checking account. Of those, 70% have never

2

had a checking account.

Compared with the US population, individuals who are financially

unengaged are the least likely to own a checking account, a savings

account, or a credit card, and they are the most likely to have never

owned these products. Individuals in this segment are among the

least likely to perform financial transactions at a bank branch, ATM,

online, or via mobile channels.

» � 0% do not have a savings account. Of those, 51% have never had

5

a savings account.

28% do not have

a checking account.

$

50% do not have

a savings account.

» � 5% do not have a credit card. Of those, 69% have never had a

5

credit card.

» � 1% have a prepaid card, and 5% have a payroll card.

1

» � 3% use online banking and 27% use mobile financial

3

services regularly.*

» � 1% use cash always or often to make purchases.

6

» � 0% pay bills in person always or often.

3

» � toring money at home is a way that 25% of this segment saves.

S

* Mobile financial services includes mobile banking, receiving an SMS alert from

�

a financial services provider, and using mobile remote deposit capture.

Regular use = in the last 30 days.

�

3) How to Reach 39 Million Unengaged Consumers

The financially unengaged have manageable debt, low levels of

financial stress, and self-awareness about the state of their

money management skills.

Providers have an opportunity to serve this segment by further

exploring their financial pain points and testing innovative solutions

to uncover:

» � hat are the most effective strategies for reaching these

W

consumers? Do partnerships with entities that have trusted

relationships with members of this segment - such as schools,

service organizations, community groups, and faith-based

communities – work, and, if so, what are the elements of

successful partnerships?

» � hat is driving the lack of awareness or engagement amongst

W

this segment? Do they not wish to engage or have they not

identified products that meet their needs? Can smart design of

default settings help individuals in this segment get the most

out of products and services without having to engage deeply or

proactively? Do smart, automated bill payment and/or saving

features appeal to this segment? Can financial services providers

connect with and help Unengaged consumers by calling out their

financial pain points and corresponding impacts?

» � an credit-building products or credit counseling services

C

provide an effective avenue for engaging this segment?

A third of this segment could not estimate their credit quality,

8% did not know they had a score, and more than half of those

who provided consent to pull their score (and were matchable by

Experian®) had a subprime or deep subprime score. Is helping

consumers build and improve their credit histories a successful

strategy for providers to build a trusted and mutually-beneficial

relationship with members of this segment?

Read More and Engage

To engage with the dialogue, follow us or use #finhealth.

@cfsinnovation

LinkedIn Facebook

Support for this Brief

MetLife Foundation is a major sponsor of CFSI’s ongoing

consumer financial health work, including these segment briefs.

About the Consumer Financial Health Study

The Consumer Financial Health Study benefited from guidance

and generous financial support from Ford Foundation and MetLife

Foundation. The Consumer Financial Health Study also benefited

from generous financial support from American Express.

The Center for Financial Services Innovation launched its

Consumer Financial Health Study to better understand the current

state of financial health in America and consumer challenges.

For more on the study – including details on the survey instrument,

methodology, financial health indicators, and financial health

segmentation – download the segmentation whitepaper:

http://bit.ly/ConsumerFinHealth

Copyright 2015

Center for Financial Services Innovation

ALL RIGHTS RESERVED

�