1) Our Perspective

THE ELECTION AND MUNIS - NOVEMBER 2016

Ronald Schwartz, CFA

Managing Director,

Senior Portfolio Manager,

Tax-Exempt

Ron is a Senior Portfolio

Manager focused on the TaxExempt Strategies. He has

worked in the investment

management industry since

1982. Ron received a B.A. in

Business Administration from

Adelphi University and is a CFA

Charterholder and a member of

the CFA Society of Orlando.

The Republican Party was a clear winner on November 8th by taking the White House,

maintaining control of Congress, and now leading the governorship of 33 states (the most in 94

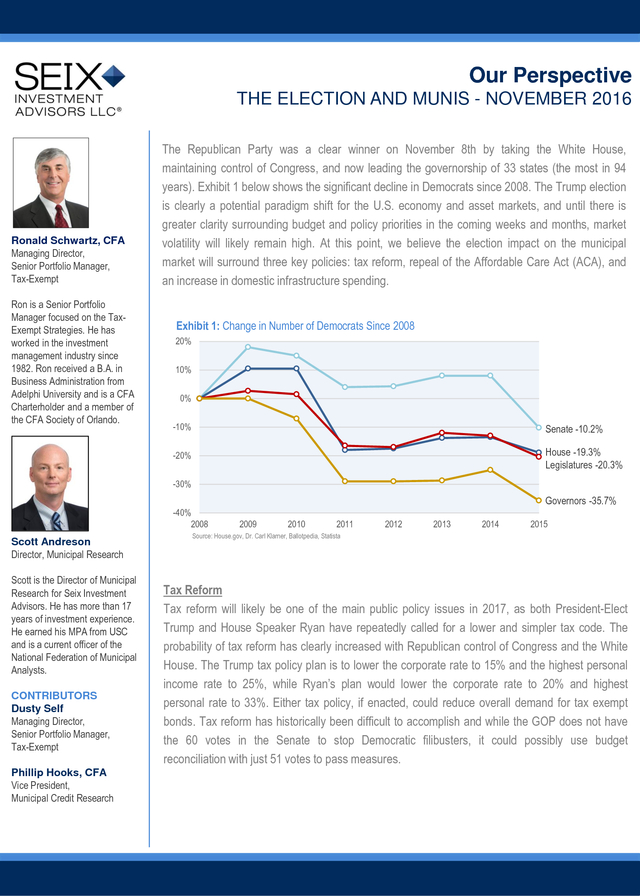

years). Exhibit 1 below shows the significant decline in Democrats since 2008. The Trump election

is clearly a potential paradigm shift for the U.S. economy and asset markets, and until there is

greater clarity surrounding budget and policy priorities in the coming weeks and months, market

volatility will likely remain high. At this point, we believe the election impact on the municipal

market will surround three key policies: tax reform, repeal of the Affordable Care Act (ACA), and

an increase in domestic infrastructure spending.

Exhibit 1: Change in Number of Democrats Since 2008

20%

10%

0%

-10%

Senate -10.2%

-20%

House -19.3%

Legislatures -20.3%

-30%

Governors -35.7%

-40%

2008

Scott Andreson

Director, Municipal Research

Scott is the Director of Municipal

Research for Seix Investment

Advisors. He has more than 17

years of investment experience.

He earned his MPA from USC

and is a current officer of the

National Federation of Municipal

Analysts.

CONTRIBUTORS

Dusty Self

Managing Director,

Senior Portfolio Manager,

Tax-Exempt

Phillip Hooks, CFA

Vice President,

Municipal Credit Research

2009

2010

2011

2012

2013

2014

2015

Source: House.gov, Dr. Carl Klarner, Ballotpedia, Statista

Tax Reform

Tax reform will likely be one of the main public policy issues in 2017, as both President-Elect

Trump and House Speaker Ryan have repeatedly called for a lower and simpler tax code. The

probability of tax reform has clearly increased with Republican control of Congress and the White

House. The Trump tax policy plan is to lower the corporate rate to 15% and the highest personal

income rate to 25%, while Ryan’s plan would lower the corporate rate to 20% and highest

personal rate to 33%. Either tax policy, if enacted, could reduce overall demand for tax exempt

bonds. Tax reform has historically been difficult to accomplish and while the GOP does not have

the 60 votes in the Senate to stop Democratic filibusters, it could possibly use budget

reconciliation with just 51 votes to pass measures.

�

2) Our Perspective

THE ELECTION AND MUNIS - NOVEMBER 2016

It’s important to note that Trump’s tax plan (unlike the

Clinton plan) does not mention the municipal tax

exemption. Even if the personal income tax rate is

lowered, there is no correlation between municipal yields

and the top marginal tax rate. Since 1980, the top

marginal tax rate has fluctuated from 70% in 1980 to

28% in 1988, and municipal rates have trended down

with Treasury rates with no change in demand for tax

exempt bonds. The most recent tax cuts of 2001 and

2003 did not impact muni rates at all (see Exhibit 2).

Finally, as we have said in the past, over 75% of the

country’s infrastructure has historically been funded by

municipal bonds, which will remain a strong headwind

against any tax reform that negatively impacts the value

of tax exemption going forward.

Exhibit 2: 10Yr AAA MMD Yield Have Followed 10YR UST Yields

Downwards and Show No correlation with the Marginal Tax-Rate…

Source: Citi Research

Infrastructure Finance

President-elect Trump envisions a $1.0 trillion infrastructure plan over 10 years that will be funded through deficit neutral tax

credits for equity investment in infrastructure projects supplemented by federal subsidized loans. Overall, the anticipated

increase in infrastructure funding is good for economic growth and public finance credit quality. Trump’s proposal is not likely to

increase the amount of municipal bond supply as the focus is on tax credits for private companies.

There were approximately $70 billion of municipal bond

proposals on the ballot this election, the largest since

2006, when about $82 billion went before voters. Just

over $60 billion of bonds were approved by voters with

the largest debt issues in California and Texas. The

uptick in borrowing is a signal that the spirit of austerity is

ending among local governments and that voters

recognize the need to fund infrastructure. New issue

supply is likely to increase, but the market should be

able to handle it as refunding issuance is likely to decline

as many callable bonds have already been advanced

refunded over the past two years.

Exhibit 3: Bond Ballot Measures Tend to Be Higher in Even Years

Source: Bloomberg

�

3) Our Perspective

THE ELECTION AND MUNIS - NOVEMBER 2016

Repeal of ACA is Negative for Hospital Bonds

Republicans are committed to “repealing and replacing” ACA and we believe the election is highly likely to have a negative

effect on the tax exempt hospital sector. In a recent 60 Minutes interview, Trump said he intended to immediately repeal

ACA. Since the election, we have seen hospital credit spreads widen out significantly as repealing or scaling back ACA

would reduce revenues for hospitals. We have an underweight recommendation to the hospital sector and we expect the

$250 billion in hospital debt to continue to underperform over the near and medium term.

The assertions in this perspective are Seix Investment Advisors’ opinion.

Investment Risks: All investments involve risk. Debt securities (bonds) offer a relatively stable level of income, although bond prices will fluctuate providing the

potential for principal gain or loss. Intermediate-term, higher-quality bonds generally offer less risk than longer-term bonds and a lower rate of return. Generally,

a portfolio’s fixed income securities will decrease in value if interest rates rise and vice versa. A portfolio’s income may be subject to certain state and local

taxes and, depending on your tax status, the federal alternative minimum tax. There is no guarantee a specific investment strategy will be successful.

This information and general market-related projections are based on information available at the time, are subject to change without notice, are for

informational purposes only, are not intended as individual or specific advice, may not represent the opinions of the entire firm, and may not be relied upon for

individual investing purposes. Information provided is general and educational in nature, provided as general guidance on the subject covered, and is not

intended to be authoritative. All information contained herein is believed to be correct, but accuracy cannot be guaranteed. This information may coincide or

conflict with activities of the portfolio managers. It is not intended to be, and should not be construed as investment, legal, estate planning, or tax advice. Seix

Investment Advisors does not provide legal, estate planning or tax advice. Investors are advised to consult with their investment processional about their

specific financial needs and goals before making any investment decisions.

Past performance is not indicative of future results.

©2016 Seix Investment Advisors LLC. Seix Investment Advisors is a registered investment adviser with the SEC and a member of the RidgeWorth Capital

Management LLC network of investment firms.

�